On February 14, 2023, EU Member States reached an agreement to update the EU list of non-cooperative jurisdictions for tax purposes. The latest update consists of 16 jurisdictions that lack commitment to improving their tax good governance or have made no progress towards their previous commitments, and are therefore included in Annex I of the EU list. These countries include American Samoa, Anguilla, the Bahamas, the British Virgin Islands, Costa Rica, Fiji, Guam, the Marshall Islands, Palau, Panama, Russia, Samoa, Trinidad & Tobago, the Turks and Caicos Islands, the US Virgin Islands, and Vanuatu. Read more

Fair taxation: agreement on minimum taxation for multinationals

The Czech Presidency of the EU Council has announced its unanimous agreement with the Commission’s proposal for a Directive, which ensures that large multinational groups pay a minimum effective tax rate. This historic agreement brings the EU closer to fulfilling its pledge to be among the first to implement the OECD tax reform. Once in effect, this agreement will introduce fairness, transparency, and stability to the international corporate tax framework. Read more

Taxation: New EU transparency rules require service providers to report crypto-asset transactions

On 8 December 2022, the European Commission proposed new tax transparency rules for all service providers facilitating transactions in crypto-assets for customers resident in the European Union.

These complement the Markets in Crypto-assets (MiCA) Regulation and anti-money laundering rules. Read more

Exportations from France

As of October 1, 2020, companies not established in the European Union (“EU”) can no longer appear as Exporter in box 2 of customs export declarations (EXA) made in France. However, in practice, French customs continued to accept companies established outside the EU to appear as exporters on customs documents. Read more

Customs importer vs fiscal importer, in France

The “direct” mode of representation is not allowed by European customs regulations for the import of goods in the name and on behalf of a company established outside the European Union (“EU”)

When you use a freight forwarder, carrier or other person established in the EU to import goods into EU territory, it is very likely that they will have offered to sign a mandate authorizing to act in the name and on behalf of your company according to the mode of “direct” representation. However, this mode of representation is only authorized by customs regulations if the person represented (endorsing the status of “declarant”) has an establishment within the EU. Read more

Electronic invoicing between taxable persons (“e-invoicing”) and transmission of information (“e-reporting”) to the French tax authorities from 1 July 2024

From 1 July 2024, businesses will face new procedures for the transmission of invoices (“e-invoicing”) and transaction data (“e-reporting”).

The application of one and/or the other procedure will depend on the place of establishment of the parties, the territoriality rules allowing to determine whether the transaction falls within the scope of application of French VAT, as well as the applicable invoicing rules.

Read more

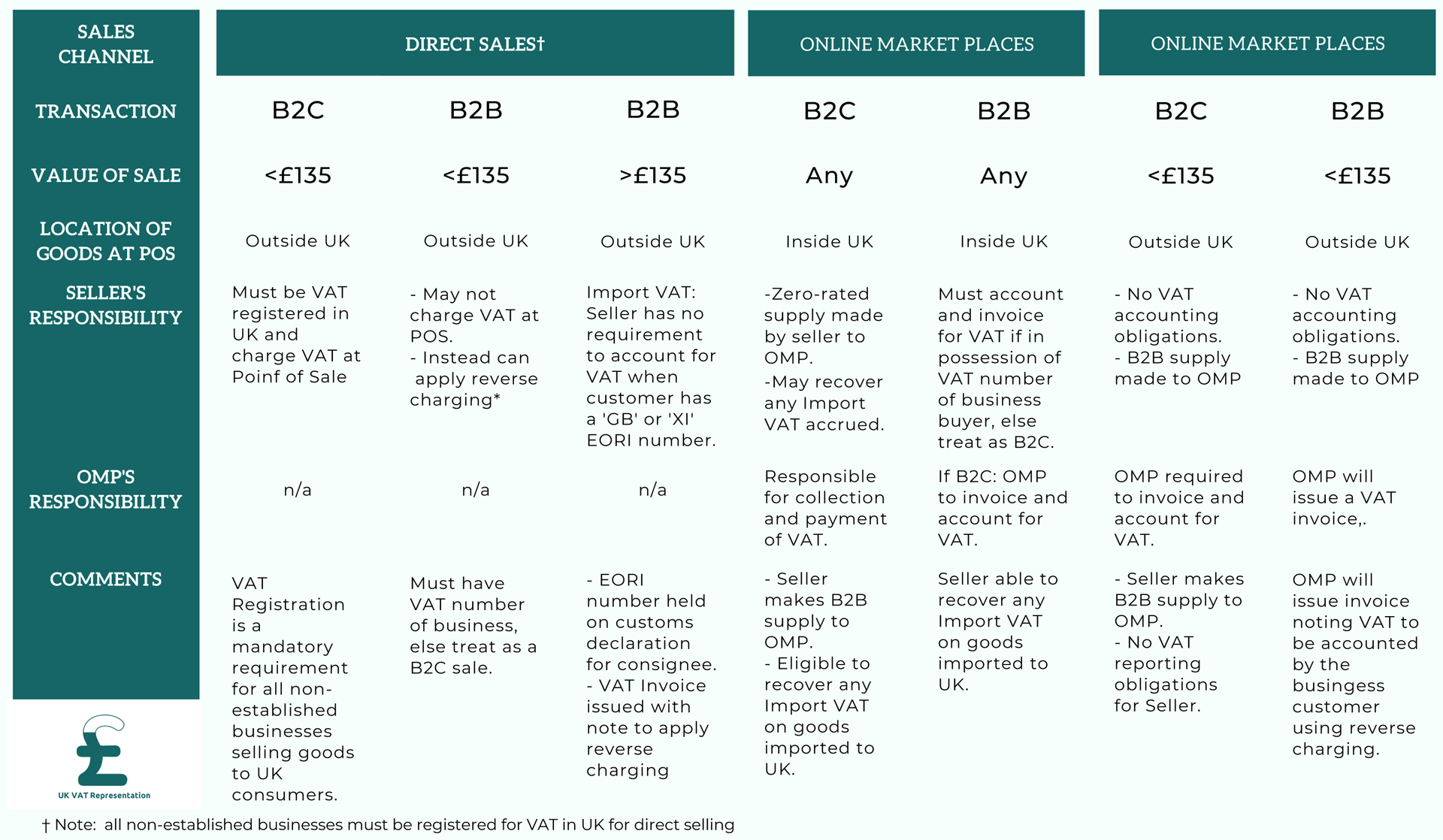

UK Distance Selling Rules in Summary

Changes to distance selling rules for the UK were implemented as part of The Taxation (Post-transition Period) Act. This document provides a summary of the changes as at 1st January 2021. Read more

La Représentation Fiscal is a founding member of the Association of French Tax Representatives

La Représentation Fiscal (LRF) is a founding member of the Association of French Tax Representatives (Association des Représentants Fiscaux Français – ARFF), a professional association with a mission to offer its Members a forum for discussion and exchange on any tax or customs subject related to the tasks of accredited tax representative. Read more

France: new way of calculating VAT for short term yacht charters

The French Tax Authorities have published a new tax bulletin on 6 November 2020, with retroactive effect from 1 November, which affects the way VAT on short term charters is calculated depending on time spent within/outside EU waters. Read more

France: Simplification of formalities related to distance sales (B2C) of excise products from January 1, 2020

Finance Law No. 2019-1479 of December 28, 2019 for 2020 has simplified the formalities relating to distance sales of products subject to excise duty.

This provision covers the sales of excise products already released for consumption in a Member State of the European Union and sent directly or indirectly by a supplier not established in France to be delivered to individuals residing in France (B2C). Read more