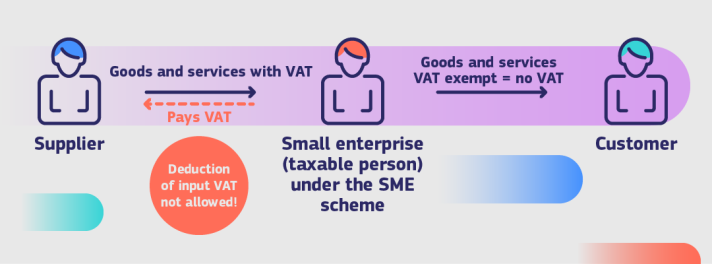

From January 1, 2025, small enterprises will be able to take advantage of a special VAT regime (SME scheme) designed to:

- Exempt their sales from VAT, allowing goods and services to be sold without charging VAT.

- Simplify VAT compliance, reducing administrative burdens.

However, businesses opting for VAT exemption will forfeit the right to deduct VAT on expenses related to their exempt sales.

Who Qualifies?

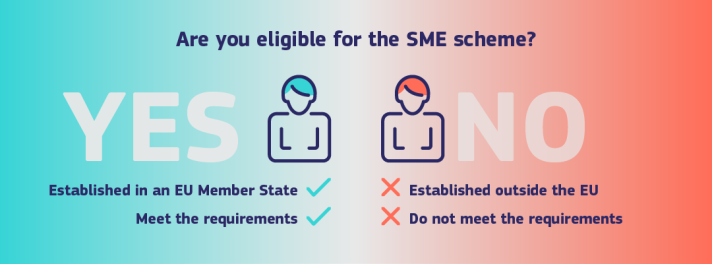

The SME scheme is available to small enterprises with a total annual turnover of up to EUR 100,000 (or the equivalent in national currency) across all Member States for both the current and previous calendar year.

- Eligibility applies in the enterprise’s Member State of establishment (MSEST) and potentially in other Member States under the cross-border SME scheme, provided those Member States have adopted the scheme in their national legislation.

- Non-EU enterprises are not eligible. This includes businesses based in the United Kingdom, even those in Northern Ireland.

Key Updates to the SME Scheme

1. New National Thresholds

Member States can set a maximum annual turnover threshold of EUR 85,000 (or equivalent) for small enterprises to benefit from VAT exemption.

- Some Member States may implement multiple thresholds for different sectors, known as sectoral thresholds.

- If a small enterprise qualifies for more than one threshold, tax authorities will determine which applies, as only one threshold can be used per business.

2. Cross-Border VAT Exemption

For the first time, small enterprises can apply for VAT exemption on cross-border transactions. This ensures equal treatment for businesses, whether they are based in the Member State where VAT is due or in another Member State.

3. Union-Wide Annual Threshold

Small enterprises with total annual turnover across all 27 EU Member States not exceeding EUR 100,000 can apply for the cross-border SME scheme.

Simplified Compliance

- Single Registration: Businesses only need to register once in their MSEST, receiving a unique identification number (EX number) valid across all Member States where they claim VAT exemption.

- Quarterly Reporting: Traditional VAT returns will be replaced by a single quarterly report, covering the enterprise’s turnover across all Member States.

- Simplified Invoicing: Invoices will be easier to manage under the new system.

Eligible Goods and Services

Most goods and services can qualify for VAT exemption, though there are specific exceptions.

Conditions for Applying

The specific conditions depend on whether a business is applying for the domestic SME scheme or the cross-border SME scheme.

For more detailed information and to assess eligibility, visit the campaign materials page or use the eligibility simulator.